Today, Maine companies that conduct business only within our states borders are at a competitive disadvantage to multi-state companies operating in Maine because of a loophole in a business tax break called the Maine Capital Investment Credit, or MCIC. Lawmakers should seize the opportunity to close this loophole and level the playing field for businesses in Maine.

The MCIC is based on federal bonus depreciation laws — a type of business tax break that allows companies to immediately write off large purchases of long-term assets in the year they are purchased, rather than over the lifetime of the asset.

A company with income from Maine only receives roughly the same benefit whether it uses the MCIC or not; The program simply front-loads tax benefits that would normally accrue over time, with the company “paying back” the up-front benefit in subsequent years.

However, the structure of the MCIC provides disproportionately large benefits to businesses with out-of-state income, compared with companies who conduct all their business in Maine. LD 1671 seeks to level the playing field by closing this unintended loophole.

For businesses that have income in Maine only, the MCIC works as intended. Those companies can choose to write off the full purchase value of capital investments worth more than $1 million in the year they are purchased and pay higher taxes in following years because they will have already used up their entire write-off.

But for businesses operating in Maine with income from other states, the accelerated, up-front benefit is never paid back in full.

A process called “apportionment” ensures businesses only pay Maine taxes on income that originated in Maine. Normally, depreciation is apportioned too, based on the amount of business activity located in the state. But a flaw in the MCIC allows companies with income in several states to claim a full-value, unapportioned Maine Capital Investment Credit while paying taxes on only an apportioned share of their income in subsequent years.

This creates a loophole that advantages businesses with income from other states over those with Maine-based income only. In some cases, the benefit to multi-state businesses can be several times that of the benefit to in state businesses. (See tables below for an example of how the loophole works, in practice.)

MECEP has previously questioned the value of the MCIC as a tool for spurring business development, particularly outside the context of a recession, we recognize that question is not before you today. However, we support a bill before legislators this session, LD 1671, because it would at least close a loophole in the program and level the playing field for all businesses making large capital purchases.

If the Legislature is not able to close this loophole, it would be on solid economic grounds to cut or eliminate the MCIC altogether. The Congressional Research Service summarized research that found the federal bonus depreciation program to be “a relatively ineffective tool for stimulating the U.S. economy during periods of weak or negative growth.”[i] Another deep study into depreciation programs found studies claiming increased investment due to bonus depreciation were actually identifying little more than a timing shift wherein companies were making investments that they already planned to make sooner to take advantage of tax benefits.[ii]

How the MCIC loophole works:

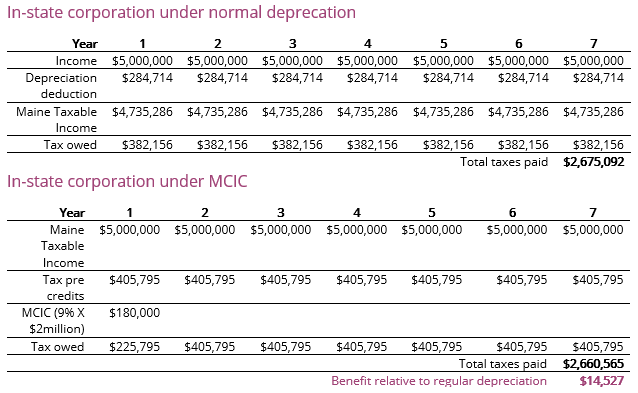

For this example, we need to consider two hypothetical companies. First, Company A, with 100 percent Maine-based income

This in-state corporation with a new $2 million piece of equipment would receive an income tax credit through the MCIC equal to $180,000, which approximates the same value as shielding $2 million in income from the top corporate tax rate of 8.93 percent. However, the company ends up paying back this credit by paying higher taxes later because they’ve already used up all their depreciation in the first year.

Assuming this company has about $5 million in taxable income, after 7 years, the difference between using normal depreciation and the Maine Capital Investment Credit is only about $14,527 even though the company’s initial tax savings is $180,000.

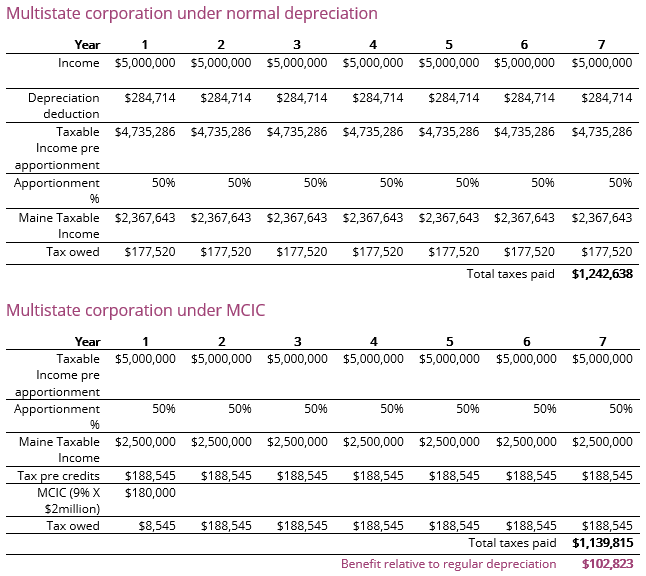

Now, consider Company B. This business has the same profile, but it operates in multiple states and derives just half its its income in Maine.

For Company B, the benefit is much different. When it makes the same $2 million equipment purchase, its MCIC benefit after 7 years relative to normal depreciation is $102,823 —seven times the benefit available to a company of the same profile, making the same investment, and strictly doing business in Maine.

Notes:

[i] Gary Guenther, “Section 179 and Bonus Depreciation Expensing Allowances: Current Law, Legislative Proposals in the 113th Congress, and Economic Effects,” Congressional Research Service, May 23, 2014.

[ii] Lily L. Batchelder, “Accounting for Behavioral Considerations in Business Tax Reform: The Case of Expensing,” draft, January 24, 2017, page 20. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2904885